5 Major Types of MPF Funds

Learn More About MPF Funds and the “JJ Five” Band

Detailed Profile Of JJ Five

Detailed Profile Of JJ Five

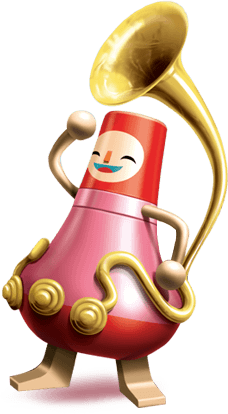

To enhance scheme members’ understanding about MPF investment and the features of the five major types of MPF funds, the MPFA has created five cartoon characters, which form the “JJ Five” Band.

|

|

|

|

High Potentialrisk |

| MPF Conservative Fund | Guaranteed Fund | Bond Fund | Mixed Assets Fund | Equity Fund |

Expectedreturn

High

| Name | Kam Ka Po (MPF Conservative Fund) |

|---|---|

| Slogan | Earning interest very slowly |

| Personality | Very conservative; definitely risk averse |

| Motto | No risk, no pain; seeking stability rather than beating inflation |

| Hobbies | Enjoys yum cha in the same restaurant every morning; likes hiding treasured items in secret places and checking them out from time to time |

| Investment Objectives | Doesn’t expect too much; targets a rate of return similar to the Hong Kong Dollar savings rate |

|---|---|

| Investment Instruments | Short-term bank deposits and short-term bonds (with an average investment period not over 90 days) |

| Risk Tolerance Level | Relatively low |

| Major Risks | Fluctuations in interest rates (i.e. when interest rates rise, bond prices may drop, which may lead to a drop in the fund price) |

| Fees & Charges |

|

| Features |

|

| Fans | My fans are conservative investors who do not like to take risks, or people close to retirement. They always say, “We’d rather earn a return below the inflation rate than take a higher risk for a higher potential return.” |

| Points to Note before Investing |

|

| Video |

|

| Name | Kam Ka Ching (Guaranteed Fund) |

|---|---|

| Slogan | Understanding the terms and conditions for guaranteed returns. |

| Personality | A born negotiator who likes to make conditional promises |

| Motto | Look before you leap |

| Hobbies | Stamp exchange, book exchange – anything involving conditional exchanges |

| Investment Objectives | Primarily to provide a guarantee on capital invested, but also to achieve a guaranteed rate of return |

|---|---|

| Investment Instruments | Bonds, stocks, or short-term, interest-bearing money-market instruments |

| Risk Tolerance Level | Relatively low, but it also depends on whether the guarantee conditions can be met when the MPF is withdrawn |

| Major Risks |

|

| Fees & Charges | The guarantor usually charges a guarantee fee or reserve charge, in addition to the basic fees and charges of most other MPF funds. |

| Features |

|

| Fans | My fans do not like taking risks, and prefer having guarantees. Some of them are close to retirement. They are willing to abide by the guarantee terms and conditions in order to get a guaranteed return. Their slogan is “agree to the terms and conditions to get the guarantee”. |

| Points to Note before Investing |

|

| Video |

|

| Name | Kam Ka Pong (Bond Fund) |

|---|---|

| Slogan | Looking for steady returns |

| Personality | Happy with the status quo; easily satisfied; will not take a huge amount of food in one helping at buffets |

| Motto | Stay calm and save money gradually |

| Hobbies | Jogs in the park regularly; enjoys relaxing in the shade of a tree |

| Investment Objectives | To earn a stable income from interest or bond coupon rates, and make a profit from bond trading |

|---|---|

| Investment Instruments | Bonds |

| Risk Tolerance Level | Low to medium |

| Major Risks |

|

| Features | The bonds must meet the minimum credit rating or listing requirements prescribed by the MPFA. |

| Fans | My fans are moderately conservative and relatively mature in age. They seek growth by playing it safe, but are willing to bear moderate risk for steady returns over the medium-to-long term. |

| Points to Note before Investing |

|

| Video |

|

| Name | Kam Ka Kwan (Mixed Assets Fund) |

|---|---|

| Slogan | The proportion of stocks and bonds determines the risk level |

| Personality | Flexible; a good planner |

| Attitude towards Life | Adjusts strategies in response to different life stages |

| Favourite Food | All dishes with dual flavours, like “yuan yang rice” (fried rice with tomato and cream sauce), sandwiches with ham and eggs, rice noodles with squid balls and fish fillet |

| Investment Objectives | To achieve capital appreciation over the long term by investing in a combination of stocks and bonds |

|---|---|

| Investment Instruments | A mix of stocks and bonds |

| Risk Tolerance Level | Medium to high, depending on the relative weight of different assets in the investment portfolio. In general, a greater proportion of stocks is associated with a higher level of risk. |

| Major Risks |

|

| Features |

|

| Fans | My fans cover a wide range of investors, from young to old, and from conservative to aggressive. They can adjust the proportion of stocks and bonds in their portfolios to suit their needs at different life stages. Generally, younger scheme members have a longer investment horizon, so they have a higher risk tolerance level. They may invest in a portfolio with a higher proportion in stocks in order to achieve a higher potential returns. |

| Points to Note before Investing |

|

| Video |

|

| Name | Kam Ka Chun (Equity Fund) |

|---|---|

| Slogan | High potential returns come with high risk. |

| Personality | Risk taker, adventurous with a good Adversity Quotient |

| Motto | No risk, no gain |

| Pet Phrase | A patient angler is rewarded with a big catch. |

| Hobbies | Sports that are challenging and fulfilling: e.g. rock climbing, white-water rafting and skateboarding |

| Investment Objectives | Relatively aggressive; aims for capital appreciation and a return higher than inflation over the long term |

|---|---|

| Investment Instruments | Stocks |

| Risk Tolerance Level | Relatively high |

| Major Risks |

|

| Features |

|

| Fans | My fans are usually young people with a long investment horizon and a higher risk tolerance level. They also include other scheme members who are risk tolerant. They understand that market movements might cause great fluctuations in fund prices. |

| Points to Note before Investing |

|

| Video |

|

What is an Index Fund? What is an Index Fund?An Index Fund is a passively managed fund. Its investment objective is to track the performance of the reference index. Investment managers of Index Funds passively track changes in the constituent stocks and market exposure of the target index to replicate the performance of the index as closely as possible. The fees for passively managed funds are generally lower than for other funds. Why does the performance of the Hang Seng Index (HSI) Tracking Fund fail to follow exactly the movement of the HSI?Although the investment objective of HSI Tracking Fund is to match as closely as practicable the performance of the HSI, there can be no assurance that the fund’s performance on each valuation day will be identical to the HSI because of different factors:

|

|