Should I Make Additional MPF Contributions?

How do I Assess whether I Need to Make Additional MPF Contributions?

As different people have different retirement needs, the amount of savings needed for retirement varies. When you assess your retirement needs, these are the key elements to consider:

- Number of years before retirement

- Monthly expenses during retirement

- Number of years of retirement (i.e. life expectancy)

- Average inflation rate

- Expected rate of return of your savings/investments during retirement

You can enter the relevant data in the Retirement Planning Calculator to calculate the MPF benefits and other savings you will have at the age of 65 and assess if the amount meets your anticipated retirement needs.

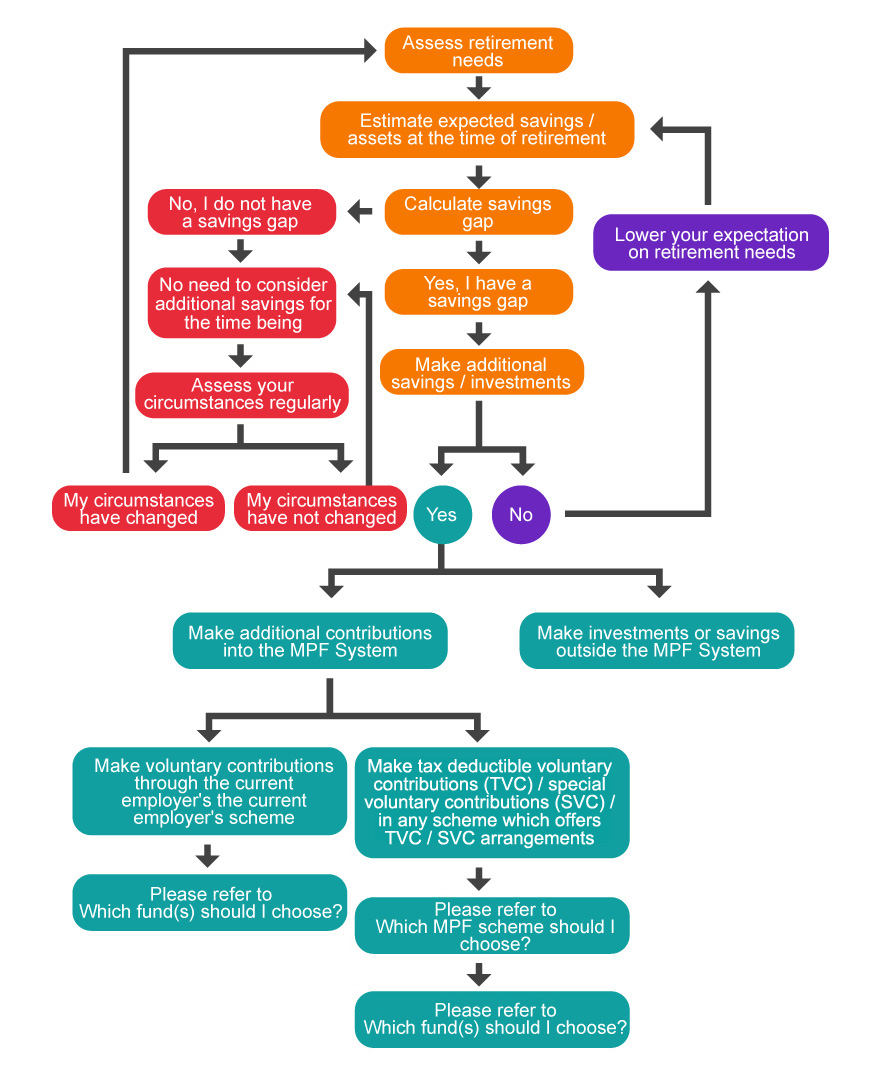

This “Decision Tree” can help you determine whether you should make additional MPF contributions or other investments/savings according to your retirement needs, MPF and other assets.

This “Decision Tree” can help you determine whether you should make additional MPF contributions or other investments/savings according to your retirement needs, MPF and other assets.

Additional MPF Contributions

| If you decide to make additional contributions, you can make not only voluntary contributions (“VC”) under the contribution account of your current employer’s scheme but also tax deductible voluntary contributions (“TVC”) or special voluntary contributions (“SVC”) in an MPF scheme which offers TVC / SVC arrangements of your own choice. All VC, TVC and SVC are additional contributions made under the MPF System, but they vary considerably in terms of how to open an account, contribution arrangements, tax incentives and other details: |

|

| VC | TVC | SVC | |

|---|---|---|---|

|

|

VC:

|

TVC:

|

SVC:

|

|

|

VC:

|

TVC:

|

SVC:

|

|

|

VC:

|

TVC:

|

SVC:

|

|

|

VC

|

TVC:

|

SVC:

|

When you consider whether to make VC or SVC, you should consider the following three factors:

Convenience:If you make contributions to the current scheme under the management of the same trustee, it will be easier to manage than opening another account with another scheme. If you choose another scheme, you would have to handle all arrangements for making contributions by yourself. |

|

Whether your employer will also make voluntary contributions:You should find out whether your employer will also make voluntary contributions. If yes, it would be better to stay in the scheme chosen by your current employer. |

|

Choice of funds:Making special voluntary contributions in another scheme of your own choice can broaden the range of funds to choose from, which may be advantageous if you feel that the range of funds in your current scheme cannot meet your desired asset allocation. |