Counting on a windfall for a worry-free retirement?

Working people often dream of getting a windfall and immediately retiring to a comfortable life. But does a windfall guarantee a worry-free retirement? Suppose you are about to retire and you win a prize of $5 million with a choice of one of three conditions attached. Which of these three fates would you choose: (1) live until your 120th birthday; (2) spend half of your assets on medical expenses; or (3) lose half of your wealth in a financial crisis in 10 years.

Working people often dream of getting a windfall and immediately retiring to a comfortable life. But does a windfall guarantee a worry-free retirement? Suppose you are about to retire and you win a prize of $5 million with a choice of one of three conditions attached. Which of these three fates would you choose: (1) live until your 120th birthday; (2) spend half of your assets on medical expenses; or (3) lose half of your wealth in a financial crisis in 10 years.Whether $5 million is sufficient for retirement varies amongst people. But the fact is that all of us face the risks related to longevity, inflation and investment when planning for retirement. If we ignore these risks, no amount of luck will make our retirement dreams come true. To effectively manage your investment risk, start by planning around the accumulation, maintenance and withdrawal of wealth for your retirement.

Accumulation: Invest a fixed amount on a regular basis

Accumulation: Invest a fixed amount on a regular basis

Instead of counting on luck, count on yourself to build a nest egg for retirement. To save your pot of gold, while minimizing the risks associated with investment, consider adopting the “dollar cost averaging” strategy. With this strategy, you invest a fixed dollar amount in a particular investment on a regular basis, buying more funds or stock units when the price is low, and fewer units when it is high, averaging out the unit cost over time. In the long term, this strategy will help you mitigate the impact of short-term market fluctuations. In fact, your monthly MPF contributions and monthly stock and fund investments all adopt this strategy to reduce investment risk.Maintenance: Adjust risks according to your age

Maintenance: Adjust risks according to your age

As you gradually accumulate wealth, to balance risks and returns, consider adopting “strategic asset allocation” as a mid- to long-term investment plan. This is a sophisticated approach, but there are some simple formulas available in the market that can be used for reference. One widely used formula is the “100-minus-age rule”, which subtracts your age from 100 to get a percentage of your portfolio that should be kept in higher-risk assets. For example, if you are 30 years old, consider making 70% of your investments in higher-risk assets. When you turn 40, it drops to 60%, and so on. Young people who have just entered the workforce have a long investment horizon. They are in a better position to invest in higher-risk products to achieve higher returns. They still have sufficient time to recover their losses in case of an economic downturn. As people approach retirement age, however, to hold onto their gains, they may consider investing in relatively low-risk products. The MPF’s Default Investment Strategy and target date funds share this approach, which automatically reduces the proportion of the scheme member’s investments in higher-risk assets, while increasing the proportion in lower-risk assets as the member approaches retirement age to strike a balance between investment risks and returns.

Young people who have just entered the workforce have a long investment horizon. They are in a better position to invest in higher-risk products to achieve higher returns. They still have sufficient time to recover their losses in case of an economic downturn. As people approach retirement age, however, to hold onto their gains, they may consider investing in relatively low-risk products. The MPF’s Default Investment Strategy and target date funds share this approach, which automatically reduces the proportion of the scheme member’s investments in higher-risk assets, while increasing the proportion in lower-risk assets as the member approaches retirement age to strike a balance between investment risks and returns. Withdrawal: Drawing down savings in an orderly fashion

During retirement, you will need to make the most of your nest egg to provide sufficient cash to cover your everyday needs. Along with continuous investing to offset inflation, you should be careful about withdrawing your retirement savings: take too much at once and your savings will run out quickly, but if you are too cautious on spending, the quality of your retirement life may suffer. Neither approach is desirable. One of the more popular approaches is the “4% rule”, which recommends that retirees withdraw no more than 4% of their savings annually. This rule is not based on a precise calculation, but is recommended by scholars with reference to long-term historical data on stock and bond returns.

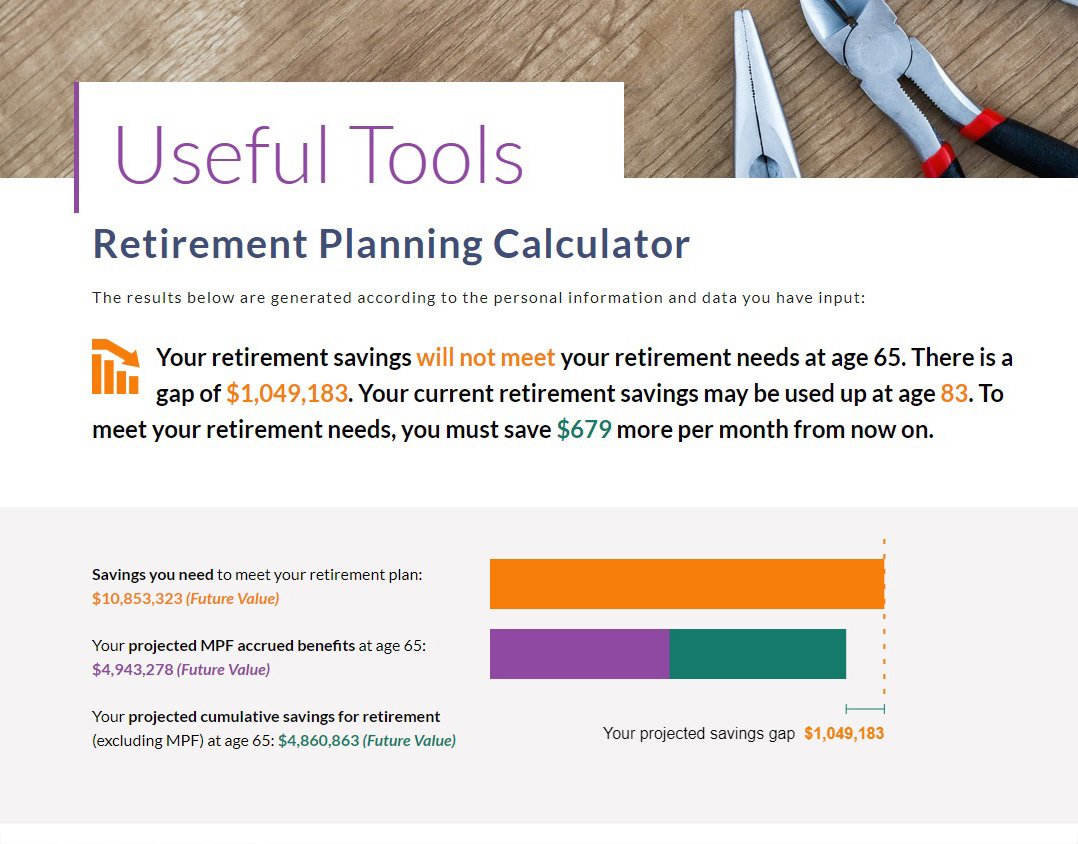

During retirement, you will need to make the most of your nest egg to provide sufficient cash to cover your everyday needs. Along with continuous investing to offset inflation, you should be careful about withdrawing your retirement savings: take too much at once and your savings will run out quickly, but if you are too cautious on spending, the quality of your retirement life may suffer. Neither approach is desirable. One of the more popular approaches is the “4% rule”, which recommends that retirees withdraw no more than 4% of their savings annually. This rule is not based on a precise calculation, but is recommended by scholars with reference to long-term historical data on stock and bond returns.Assuming the returns on your annual investment can offset inflation, a 4% annual withdrawal rate means your savings will cover your needs for 25 years. The essence of the rule, however, is not the specific percentage, but withdrawing your savings in an orderly fashion. You can also withdraw your accrued MPF benefits in a lump sum or by instalments. To help determine how large a nest egg you need to ensure that your savings will meet your needs, use online tools, such as the Retirement Planning Calculator provided by the MPFA.

You need more than just a large nest egg to retire worry-free. You also need a sound risk management strategy for your retirement investment. This includes saving or investing a fixed amount on a regular basis, adopting an appropriate asset allocation strategy, and during retirement, withdrawing your savings in an orderly fashion and continuing to make proper investments. With a little forethought, you won’t need a windfall to achieve a comfortable retirement life.

Kenny Mak – Chartered Financial Analyst

Click here to series of “Overcoming blind spots for a happy retirement”

Click here to series of “Overcoming blind spots for a happy retirement”